By Jemimah Wellington, JKNewsMedia Reporter

NIGERIA’s ECONOMY is receiving significant boosts from two major investments in the oil and maritime sectors.

This is reflecting growing international confidence in the country’s reforms.

ExxonMobil has announced its intention to invest $10 billion into Nigeria’s deep-water oil projects, marking a major step forward in the nation’s energy landscape.

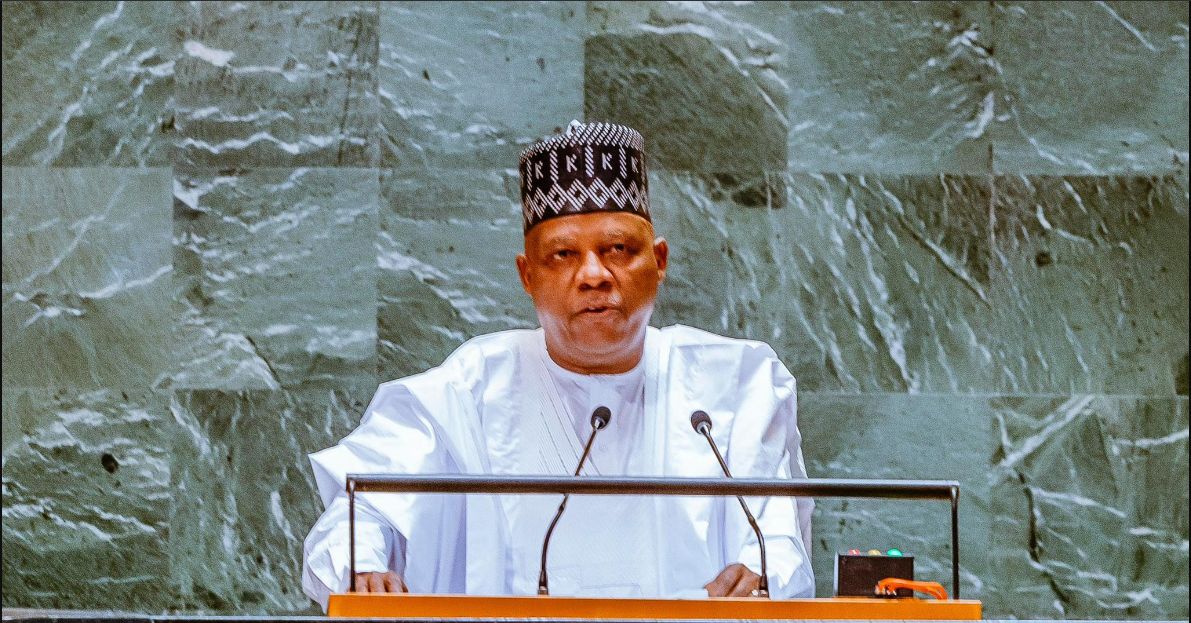

The disclosure was made during a high-level meeting at the ongoing United Nations General Assembly (UNGA) in New York.

The meeting included key Nigerian government officials, such as Vice President Kashim Shettima, who expressed optimism about the development.

The investment is also seen as a direct response to Nigeria’s recent economic reforms aimed at fostering a more business-friendly environment.

Vice President Shettima highlighted the ongoing initiatives under President Bola Ahmed Tinubu’s administration to improve the ease of doing business.

These efforts include unifying the exchange rate, removing fuel subsidies, and implementing tax reforms.

Shettima emphasized that these changes, though challenging, are designed to create a more predictable and stable business climate for investors.

A statement signed by Stanley Nkwocha, Senior Special Assistant to The President on Media & Communications, (Office of The Vice President) on Thursday, 26th September 2024, reveals that ExxonMobil’s planned investment centers around the Owo subsea project, a deep-water initiative that could drastically increase Nigeria’s oil output.

This project is expected to inject $1 billion annually into maintenance and production, with a targeted 50,000 barrels per day increase over the coming years.

ExxonMobil’s Shane Harris, Chairman and Managing Director of its Nigerian affiliates, reiterated the company’s commitment to Nigeria, noting its 70 years of oil production history and the production of over 8 billion barrels to date.

Meanwhile, DP World, a global leader in maritime logistics, has revealed plans to develop a multibillion-dollar port project in Nigeria.

It says this initiative is set to enhance Nigeria’s infrastructure and trade capacity, making the country a central hub for maritime operations in Africa.

Also, the proposed port project aligns with President Tinubu’s efforts to attract foreign investments and modernize Nigeria’s trade systems.

Sultan Ahmed bin Sulayem, Group Chairman and CEO of DP World, outlined the company’s vision to bring capital, expertise, and resources to Nigeria.

With its extensive global supply chain network, DP World intends to tap into Nigeria’s underutilized potential, boosting both import and export operations.

Vice President Shettima welcomed DP World’s plans, describing it as evidence of Nigeria’s improving economic climate and the government’s commitment to fostering foreign investments.

The administration has pledged its full support for these investments, signaling a new era of economic growth and global collaboration for Nigeria.

The VP added that these investment commitments signal a strong vote of confidence in Nigeria’s economic policies, as both ExxonMobil and DP World prepare to make long-term contributions to the nation’s oil and maritime sectors.

He also assures that the country continues to position itself as an attractive destination for international investors, with more sectors expected to benefit from ongoing reforms.

At JKNewsMedia, our dedication to delivering reliable news and insightful information to our cherished readers remains unwavering. Every day, we strive to provide you with top-notch content that informs and enlightens. By donating to JKNewsMedia, you directly contribute to our mission of delivering quality journalism that empowers and informs. Your support fuels our commitment to bringing you the latest updates and in-depth analysis. Let's continue to uphold the highest standards of journalism and serve our community with integrity and dedication. Thank you for being a part of the JKNewsMedia family and for your ongoing support.